It’s extremely common that financial advisors tell you to buy bond funds for income. This is bad advice and most advisors don’t even know it. Recall that there is no required education for being a financial advisor. The only requirement is passing a simple multiple-choice test that any sixth-grader could pass.

If you want investments to generate income, by individual bonds, not bond funds.

Individual bonds have two fantastic benefits:

- they pay a fixed income that is the same year in and year out. That income never changes regardless of market conditions

- every bond has a specific maturity date at which time you get the full face value of the bond

Every conservative investor wants those two benefits.

However, the moment you put a bunch of bonds into a fund, those two benefits disappear. The interest rate is no longer fixed as the fund manager will buy and sell bonds over time and the interest income will change. Additionally, because there are many bonds in the fund, there is no maturity date when you are promised to get your principal returned.

Not only do you lose these two benefits of individual bonds, but you also take on some additional risks.

Since there is no specific maturity date, you will get whatever the fund shares are worth on the day that you sell. You may make a profit or you may have a loss. If you invest today, in July 2019 The probability of having a loss is greater than the probability of having a profit. Why?

Because interest rates are historically low right now. When interest rates rise, the value of your bond funds will fall. So if you believe that interest rates will rise in the future, do not invest in bond funds and get your money out of bond funds now. Instead, by individual bonds.

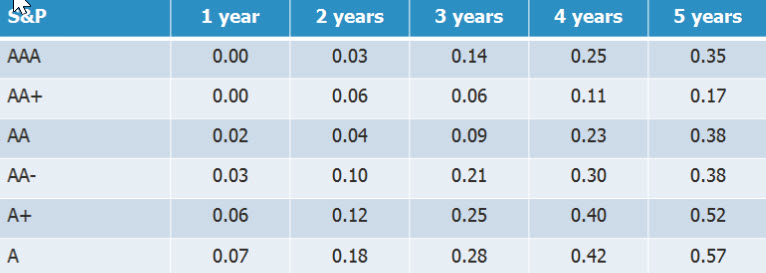

Financial advisors will tell you that if you by individual bonds you will not be diversified and you will have more risk. The answer to this is simple. Only by high-quality bonds where you do not have a risk of default. By bonds rated A or better. Far less than 1% of such bonds every default. (Note-default does not mean investors lost money. Default is a tracking of any missed payments by the bond issuer).

Global S&P cumulative default rates

Want to understand more?